Mar 20, 2025

How Indian Banks Can Leverage Verification APIs for Faster Lending Decisions

Indian banking is undergoing a digital transformation, especially in lending. Traditional loan approval processes are being reinvented with digital verification solutions that enable faster and more secure lending decisions. These verification solutions act as digital bridges, connecting banks to various trusted data sources – government databases, credit bureaus, and financial institutions – to instantly validate borrower information. By integrating directly with systems like Aadhaar (the national ID database), PAN (tax ID) records, credit bureau scores, payroll data, and bank account data, lenders can automate checks on identity, income, employment, and credit history within seconds. The result is a drastic acceleration in loan processing and a tighter clamp on fraud. According to an RBI report, around 70% of all digital loans in India are now approved and disbursed within 24 hours, a testament to how verification APIs have collapsed timelines that once spanned weeks. This speed is vital as the Indian digital lending market is booming and is projected to reach $515 billion by 2030, and customers demand instant services.

Equally important, verification APIs strengthen security in an era of rising financial fraud. In 2023-24, financial fraud in India surged, costing businesses over ₹14,000 crore. By cross-verifying applicant data against official sources in real time, banks can catch inconsistencies or fake credentials early. For instance, a PAN (Permanent Account Number) verification API can flag a counterfeit PAN card by checking it against the government database, drastically reducing the risk of identity theft and financial fraud. In short, verification APIs have become crucial tools in modern Indian banking – speeding up lending decisions while making them far more secure and compliant.

The Evolution of Lending Verification Processes

Not long ago, loan verification was a slow, manual affair. Bank officers had to physically check borrower’s documents, make phone calls or visits for in-person employment verification, and painstakingly enter data into systems. Each step was prone to delays and human error. It was common for banks to take 35-40 days to process a loan application from start to finish under these legacy methods. Consider a typical scenario - verifying a borrower’s income might involve contacting their employer and waiting for an HR letter, while KYC checks mean comparing photocopied IDs and addresses. These laborious verifications created bottlenecks that stretched approval timelines and often frustrated customers.

Today, the contrast could not be sharper. API-based verification has turned weeks into minutes. Lenders now leverage secure APIs to automatically fetch and confirm data that once required manual effort. Fintech lenders in India often approve loans in under 10–30 minutes, thanks to instant digital checks. Behind the scenes, algorithms ping multiple databases at once – confirming identity details, pulling credit scores, and analyzing bank statements – all without human intervention. Traditional banks, burdened by rigid procedures and legacy systems, used to take days or even weeks to approve a loan, but with modernization, many are catching up by adopting these APIs. The end-to-end loan origination process has shrunk dramatically: what previously took over a month can now be accomplished in a single day or even in real-time. This evolution from paper and phone calls to seamless digital verifications has eliminated manual errors and freed up banking staff for higher-value work, while borrowers benefit from near-instant approvals.

Core Components of Verification API Ecosystems

Modern lending verification isn’t a single tool but an ecosystem of specialized APIs working in concert. The core components include:

Identity Validation APIs

These APIs instantly authenticate a customer’s identity by integrating with government databases and advanced fraud checks. For example, banks use Aadhaar verification APIs to confirm an applicant’s identity via India’s biometric ID system. With simple OTP-based consent, the API pings UIDAI to verify the person’s Aadhaar details in seconds. Similarly, PAN card verification APIs validate the PAN to ensure the PAN is genuine and not blacklisted. This real-time cross-check against official data makes it nearly impossible for someone to use a fake or stolen identity. In fact, a secure PAN API can provide instant validation and flag discrepancies, acting as a digital shield against identity fraud.

Financial Health Assessment APIs

Beyond identity, banks need to assess a borrower’s financial stability – how much they earn, spend, and can repay. Financial Health APIs help paint this 360° picture by leveraging open banking and data aggregation. With India’s Account Aggregator framework (a consent-driven financial data-sharing system), lenders can use APIs to fetch an applicant’s bank statements, transaction history, and even ITR in a standardized digital format. Instead of relying solely on credit scores, these APIs let banks analyze cash flow, income consistency, and spending habits directly from the source. For example, a Bank Statement Analyzer API can ingest months of transaction data from various bank accounts and instantly summarize metrics like average monthly salary credits, total EMI obligations, rent payments, and any bounced transactions. This offers a granular view of the borrower’s income stability and financial behavior. TartanHQ’s own Bank Statement Analyser API exemplifies this, as it can “analyse bank statements to determine credit worthiness, detect fraud, and make informed lending decisions.”

Operational Impact on Lending Institutions

The adoption of verification APIs is yielding tangible benefits for banks and NBFCs in India. Data shows that embracing automation in verification leads to: faster decision-making, reduced fraud losses, lower operational costs, and a better customer experience. By cutting out manual steps, banks can handle far more loan applications in the same amount of time, boosting their lending volumes without needing a proportional increase in back-office staff.

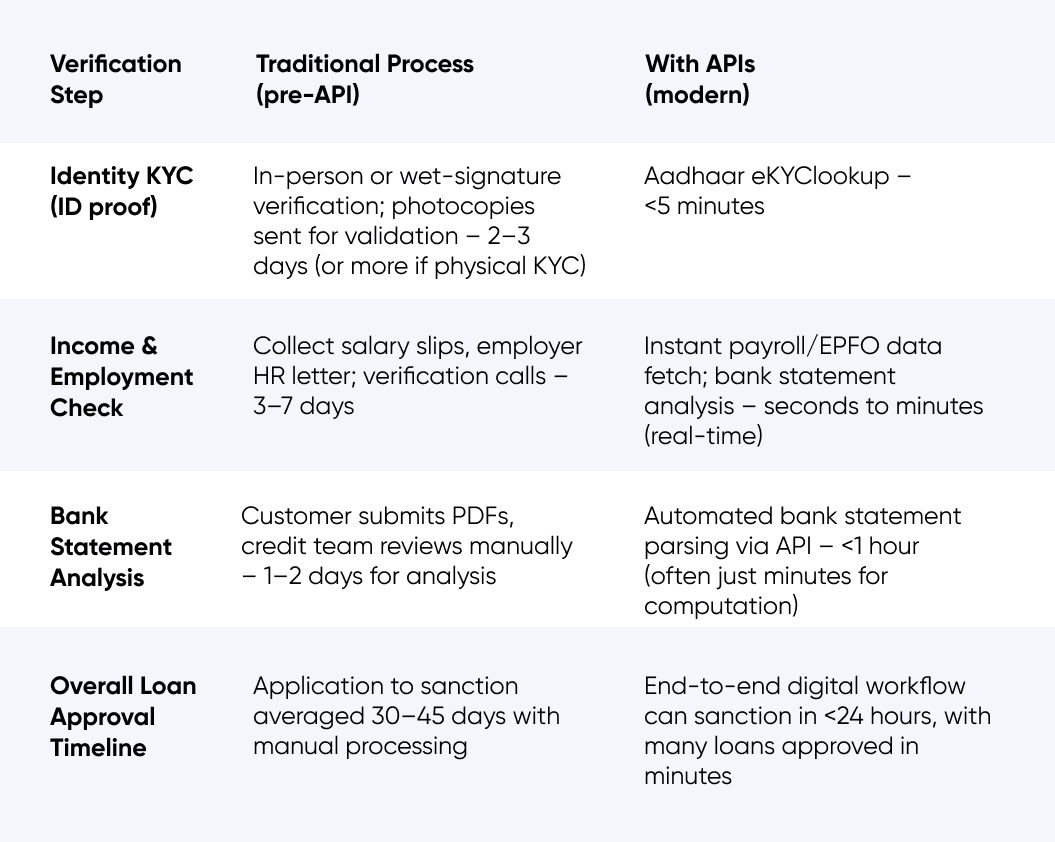

One major impact is the acceleration of loan turnaround times. We’ve gone from multi-week loan approvals to near-instant approvals for eligible borrowers. This speed gives institutions a competitive edge and delights customers. For instance, implementing eKYC and income APIs has enabled some lenders to approve personal loans within hours or even minutes, whereas before, a customer might wait over a month for a verdict. The table below highlights how verification APIs have slashed processing times at various stages:

Table: How Verification APIs Reduce Loan Processing Times in India.

As shown above, each verification component has seen an order-of-magnitude improvement. These efficiency gains translate directly into cost savings and higher productivity. Banks can process far more applications with the same resources or reallocate staff to more strategic roles (like underwriting complex cases) rather than rote document checking. One striking statistic from India’s Economic Survey is that using digital infrastructure like Aadhaar eKYC has reduced the cost of KYC compliance from about ₹1,000 per customer to just ₹6. That’s a massive drop in operational cost per loan, thanks to API-driven verification. Multiply those savings across millions of customers, and it significantly boosts a lender’s bottom line.

Fraud prevention is another area of improvement. Automated verification leaves fewer gaps for fraudsters to exploit. Error rates plummet because APIs return exact data from official sources, avoiding the typos or oversight that manual data entry can introduce. And because checks are done in real-time for every application, suspicious signals are caught immediately – whether it’s an ID that doesn’t match government records or a bank account that isn’t actually in the borrower’s name. Many banks report that integrated verification has reduced instances of loan fraud and defaults, as unqualified or misrepresenting applicants get filtered out at the application stage. Overall portfolio quality improves when lending decisions are based on verified facts rather than unverified claims on paper.

Crucially, the customer experience is vastly improved. Borrowers no longer endure a cumbersome vetting process; instead, they provide consent for the bank to fetch data and often receive a decision almost instantly. This smooth digital journey increases customer satisfaction and trust. It also means less drop-off – borrowers are less likely to abandon their application due to delays or excessive document demands. In a country where many credit-worthy individuals were deterred by complex loan procedures, APIs are helping bring more people into the formal credit system through a friendly, quick process.

Real-World Use Cases

Indian banks and fintechs have started reaping these benefits. A prime example is the government-supported PSB Loans in 59 Minutes platform, which has set a benchmark for rapid lending. This online system for MSME and retail loans integrates with various government and financial databases via APIs. It pulls an applicant’s GST returns, income tax filings, and last 6 months’ bank statements automatically and uses that data to judge loan eligibility – all in about an hour. By the time a borrower completes the online form, the system has already verified their financials and KYC through these integrations, enabling participating public sector banks to issue in-principle approvals almost instantly. This would have been unthinkable in the era of manual verification, but API connectivity to government data (GSTN, IT dept, etc.) made it possible.

Private banks are also leveraging verification APIs in their digital lending initiatives. Axis Bank, for instance, now uses the Account Aggregator network to retrieve applicants’ bank statements directly (with consent) for products like personal and auto loans, eliminating the need for customers to upload PDFs or physical statements. ICICI Bank has integrated similar APIs for credit card issuance and other retail loans, allowing them to assess incoming customers’ finances on the fly by fetching data from other banks. These early adopters report significantly faster loan disbursals and improved user onboarding. Another use case is the widespread adoption of e-KYC APIs for account opening and loans – almost all major banks (HDFC, SBI, Kotak, etc.) allow customers to complete KYC through Aadhaar-based APIs or video KYC, which feeds into lending as well by instantly verifying identity and address. This has especially exploded for personal loan apps and credit card issuance, where fully digital KYC and verification mean approval in minutes.

Fintech lenders such as Bajaj Finserv, EarlySalary, and Paytm Loans have built their platforms entirely around API-based verification, often partnering with specialist providers. They use income verification APIs to check salary deposits in applicants’ bank accounts (sometimes via penny-drop verification or account aggregator) and employment verification services that tap into databases like the EPFO to confirm a person’s employer and tenure. These checks happen behind the scenes in seconds during the loan application flow on a mobile app. The end result is that a salaried professional can get a small personal loan on their phone almost immediately after applying because all the time-consuming verifications are handled by machines. This agility has pressured traditional banks to invest in the same technologies to keep up. As an industry analyst insightfully noted, web-based lending startups process and approve loans in minutes by leveraging data and AI, whereas legacy banks’ manual processes made customers wait weeks. Now, banks are closing that gap by deploying the very verification APIs that fintechs pioneered.

TartanHQ’s Verification Solutions for Banks

To implement these advanced verifications, banks often turn to fintech partners that specialize in API solutions. TartanHQ is one such provider offering a suite of verification APIs tailored for the Indian banking sector’s needs. TartanHQ’s platform is designed to plug into a bank’s existing systems (via simple REST APIs) and provide ready-made connectivity to a variety of data sources with consent management and compliance built-in. Here’s an overview of TartanHQ’s core API offerings that can help banks optimize their lending operations:

Income and Employment Verification API

TartanHQ’s Income & Employment Verification API enables lenders to instantly verify a borrower’s stated income and job status. Rather than relying on paper salary slips or manual calls to employers, this API can fetch authenticated data on the applicant’s income streams. It works through multiple channels:

Payroll data: With the user’s consent, the API can connect to payroll systems or HRMS databases of companies to retrieve information like monthly salary, employer name, and years of employment. TartanHQ has integrations that “verify income and employment of a user by fetching payroll data to assess creditworthiness”, automating what used to require manual proof.

Bank salary credits: The API can also analyze the customer’s bank transactions (via account aggregator or bank statement upload) specifically to identify salary deposits. This confirms not only the income amount but also regularity (e.g., salary coming on the 1st of every month).

EPFO and UAN checks: For additional confidence, TartanHQ’s solution hooks into the Employees’ Provident Fund Organization (EPFO) database. By using the borrower’s PAN or UAN (Universal Account Number), it can pull their contribution history. A steady EPF contribution is a strong indicator of stable employment. In fact, TartanHQ recently introduced a feature where, with just the applicant’s mobile number, lenders can retrieve the complete employment history via EPFO records (past employers, tenure at each, etc.) through a consented pull – no more waiting for the borrower to upload experience letters.

By combining these data points, the Income & Employment Verification APIs give a comprehensive, real-time view of the borrower’s earning capacity and job stability. For example, a bank can confirm within seconds that an applicant works at XYZ Pvt Ltd, has drawn a ₹75,000 salary consistently for 12 months, and even see if they switched jobs recently. This not only speeds up the approval (no back-and-forth for documents) but also helps in risk assessment (a stable earner is a safer bet). It’s a powerful tool for underwriting, especially for personal loans, credit cards, and other unsecured loans where income validation is crucial. Banks like to use such APIs to reduce fraud (catching fake employment claims) and to extend credit to first-time borrowers by trusting data over lack of credit history. In short, TartanHQ’s API acts as a digital employment reference check and income proof all rolled into one, delivered instantly.

Bank Account Validation API

When disbursing a loan, one basic need is to ensure the bank account provided by the customer is valid and, indeed belongs to them. TartanHQ’s Bank Account Validation API handles this by offering real-time bank account authentication. Traditionally, banks used “penny drop” – depositing a small amount (like ₹1) to the account and verifying if the name matches. TartanHQ’s solution improves on this with a “pennyless” verification method, meaning it can verify the account holder’s name and status without any trial deposit. The API integrates with banking networks to confirm details using the account number and IFSC code.

This API essentially answers the question: Is this account real and active? Does it belong to the loan applicant? All in a fraction of a second. When a borrower enters their bank account details for disbursement, the API pings the relevant bank through secure channels to fetch the account holder’s name (and, in some cases the status like active/dormant). The lender’s system can then automatically check that the name on the bank account matches the loan applicant’s name on record – preventing situations where funds might go to the wrong person or a fraudulent account. TartanHQ’s product update notes that this digital process reduces verification timelines from a few days to just a few seconds. Indeed, compare the old way: a lender might wait 2-3 days for an electronic funds transfer to bounce back or be confirmed, versus now the API instantly confirming account validity on the spot.

Another advantage is bulk verification. When processing high volumes of applications or doing KYC refreshes for existing customers, the API can verify thousands of accounts programmatically, far quicker and more accurately than a manual process. This ensures there are no errors in account details that could lead to failed loan disbursals or repayment issues later. By using the Bank Account Validation API, banks dramatically reduce payout errors and fraud (no one can mislead the system by giving an account under a different name), and they enhance the customer experience (no need to wait for test deposits). It’s an example of a small but critical step in lending that, when automated, brings huge efficiency gains and fraud mitigation. TartanHQ’s penniless verification is also cost-effective since it avoids any transaction fees and operational overhead of handling the reconciliation of penny drops. In summary, this API ensures “the right person gets the money” in real-time, which is a cornerstone of secure digital lending.

Aadhaar and PAN Verification API

Compliance and fraud prevention start with solid KYC. TartanHQ provides identity verification APIs for Aadhaar and PAN that allow banks to instantly confirm a customer’s identity details as part of loan onboarding. The Aadhaar Verification API connects to UIDAI’s system to authenticate the borrower’s Aadhaar number (with user consent via OTP) and fetch e-KYC data (name, address, etc.). This lets the bank confirm that the person is genuine and their details match what’s in the Aadhaar database. It’s a quick, paperless way to satisfy proof of identity and address. Using Aadhaar in this way has been a game-changer in India, as it replaces the need for physical documents and in-person verification. TartanHQ’s Aadhaar API offering emphasizes preventing identity fraud while making onboarding easy. By catching mismatches (say, if someone tries to use an Aadhaar number not their own), it stops potential fraudsters from exploiting the system.

The PAN Verification API is equally important, especially since PAN is mandatory for financial transactions and is linked to credit histories. TartanHQ’s API checks the provided PAN against the government’s database (NSDL) to ensure it is valid, active, and corresponds to the applicant’s name and birthdate. This instantly flags fake PAN cards or mismatched PAN details that could indicate identity theft or someone trying to assume another identity’s credit profile. According to TartanHQ, verifying PAN details via API helps prevent fraud associated with fake PAN cards and ensures regulatory compliance during customer onboarding. It also automatically captures the verified PAN info for the bank’s records, which is useful for things like pulling the credit bureau report (since credit bureaus use PAN as an identifier).

Together, Aadhaar and PAN verification APIs enable a fully digital KYC process that meets RBI’s requirements. They ensure the borrower is who they claim to be and that their key ID numbers are correct. This is not only critical for compliance (e.g., satisfying the Officially Valid Document norms in KYC) but also sets the stage for other verifications (for instance, a wrong PAN would fetch the wrong CIBIL score, etc.). By integrating these APIs, banks can perform KYC in seconds during the online application flow, with no drop in user experience. In fact, customers often just input their Aadhaar or PAN and see it auto-validated almost immediately.

Implementing Roadmap for Banks

For banks, especially established ones with legacy systems, adopting verification APIs requires a clear strategy. Below is a roadmap and best practices to ensure a smooth integration:

1. Define Use Cases and Requirements: Banks should start by identifying which parts of their lending workflow will benefit most from API integration. Is the priority to speed up KYC? To automate income verification? To improve credit risk modeling with more data? By mapping pain points (e.g., KYC delays or high verification costs), the bank can prioritize the API solutions needed (Aadhaar, PAN, account aggregator, etc.). It’s also important to consider scale and types of loans – e.g., instant personal loans might need all three (identity, income, bureau) verifications in real-time, whereas a gold loan might primarily need KYC API plus a collateral check.

2. Choose the Right API Partners or Build In-House: Many banks partner with specialist fintech API providers like TartanHQ. Key considerations when choosing are compliance, reliability, and coverage of data sources. Banks must ensure any third-party API complies with RBI’s data privacy and security requirements (for instance, Aadhaar eKYC can only be done by regulated entities). The chosen APIs should have high uptime and quick response times, as they’ll be in the critical path of loan processing. Some banks might opt to build certain connectors in-house (if they have the tech resources), but partnering can drastically cut down development time since providers offer ready-to-use solutions.

3. Sandbox Testing and Pilot: Before full-scale rollout, it’s prudent to test the integration in a sandbox environment. An API provider must offer testing sandboxes where the bank’s IT team can simulate requests and responses. During this phase, banks should test for accuracy (are the APIs returning correct verifications?), performance (can they handle peak loads?), and error handling (how are exceptions or mismatches flagged?). Once satisfied, a pilot program can be run – for example, using the new verification APIs for a particular product line or a small percentage of applications initially. This pilot helps iron out any kinks in real-world conditions and also allows training of staff on the new process.

4. Integrate with Legacy Systems Carefully: Many Indian banks run on core banking and loan origination systems that are older and not naturally built for external API calls. Integration can thus be challenging. In some cases, a middleware or API gateway is deployed to bridge the gap – this layer can translate API responses into a format the legacy system accepts. As noted in industry reports, legacy systems might lack the flexibility to support modern APIs, sometimes requiring custom solutions or upgrades. Banks should consider approaches like “encapsulation” (wrapping legacy functions with API layers) or using robotic process automation as a stopgap to interface with older systems. The goal is to ensure the verification API calls become an embedded part of the workflow (e.g., as soon as an application is submitted, triggers go out to Aadhaar/PAN, etc., and responses are logged in the loan processing system).

5. Security and Data Privacy by Design: When integrating verification APIs, security is paramount since sensitive personal data is in transit. Banks should use secure encrypted channels (HTTPS with strong ciphers, VPN or dedicated lines for certain government connections). It’s advisable to never store raw data unnecessarily – for instance, if you fetch an Aadhaar XML, use it to extract needed info and then dispose of it, rather than keeping a copy of someone’s biometric ID info. Compliance with India’s new Data Protection law (DPDP) and other guidelines must be ensured. API contracts should guarantee that data fetched is used and stored in permitted ways. TartanHQ’s guidelines, for example, stress robust encryption and compliance. Banks should also build consent mechanisms (where required) – e.g., have the user check a box, or OTP authorize that their data can be pulled, to stay transparent and lawful.

6. Training and Change Management: Even with automation, bank employees will interact with the new systems. It’s important to train loan officers and operations staff on how the new verification process works. They should understand the indicators on their screens (such as “KYC verified via UIDAI” or an income verification confidence score) and know how to handle exceptions (for example, if an API returns that PAN is not found, what is the protocol? Do they ask the customer for clarification or fallback to manual verification?). Clear guidelines will ensure humans and APIs work in harmony.

7. Monitor, Optimize, and Scale: After implementation, continuously monitor the performance of verification APIs. Track metrics like success rates, any error frequencies, time saved, and improvement in approval rates or reduction in fraud cases. This data will help demonstrate ROI to stakeholders. It will also highlight if any API is underperforming or causing delays. Optimization could include tweaking the sequence of calls (some banks run certain checks in parallel to save time, for example, fetching credit score and bank statements simultaneously) or fine-tuning risk rules based on richer data (e.g., using machine learning on bank transaction data to improve credit scoring). Once the system is stable, the bank can scale up the usage to more products and even explore advanced APIs (for example, adding a vehicle RC verification API for auto loans, GST verification for business loans, etc., if not already in use).

By following this roadmap, banks can integrate verification APIs smoothly into their lending workflows with minimal disruption and maximum gain. The key is to address technical integration challenges upfront, adhere to security/compliance requirements, and bring the organization along through training and pilots. Many have done it successfully – and those who have are now able to process loans faster and more safely than ever before. The investment in integration pays off multi-fold in agility and cost savings.

Future Innovations in Verification APIs

The journey of verification APIs is far from over – in fact, it’s accelerating. Looking ahead, several cutting-edge innovations are poised to further transform how lending verification is done:

AI-Powered Predictive Analytics: Today’s APIs provide data and basic verification, but the next step is layering Artificial Intelligence to derive deeper insights and predictions. We are already seeing early signs of this: machine learning models that analyze patterns in bank transaction data to predict a borrower’s future cash flow or risk of default, beyond what a static credit score can tell. In the near future, AI could combine diverse data (income trends, expenditure patterns, social media signals, etc.) in real-time to predict creditworthiness, even for those with thin credit files. For example, an AI might detect that an applicant’s income has been increasing year-over-year and that they have low spending volatility – indicating a lower risk profile than their raw salary might suggest. Conversely, AI might flag subtle signs of financial stress (like frequent short-term loans or gambling expenses in bank statements) that wouldn’t be evident from traditional verification. These predictive analytics could be exposed via APIs to lenders, effectively giving a “risk score 2.0” or recommended loan terms dynamically calculated for each applicant. The goal is to make credit decisions not just on current verified data but on forward-looking predictions, which can increase approval rates safely and personalize interest rates. AI will also continue to improve fraud detection – for instance, spotting anomalies in document submissions or detecting synthetic identities by correlating data points. As one industry blog predicted, integration of AI will enable smarter fraud detection and more trustworthy verification ecosystems. We can expect verification APIs to increasingly come with built-in AI insights, not just raw data.

Blockchain and Decentralized Verification: Blockchain technology offers the promise of tamper-proof, sharable verification records. Imagine a world where a borrower’s identity credentials, employment certificate, and credit history are all stored as verifiable credentials on a blockchain. Instead of each lender verifying everything from scratch, a borrower could grant a lender access to their secure digital identity wallet where these credentials are already verified by trusted issuers (for example, their diploma from a university, employment by a previous employer, or a credential agency, etc.). The lender’s verification API of the future might simply check the authenticity of these credentials on the blockchain (which is cryptographically assured) and instantly get the needed assurance. This concept, known as self-sovereign identity (SSI), could drastically cut duplication in KYC across institutions. A few pilot projects in India and globally are exploring blockchain-based KYC shared between banks. Likewise, land records and asset registries on blockchain could speed up collateral verification for loans – if property ownership is recorded in a blockchain ledger, a lender’s system could instantly verify lien status and ownership without lengthy title searches. Blockchain can ensure that once a document is verified, it’s locked against alteration, thereby creating a trail of trust. Indian regulators have shown interest in blockchain for simplifying KYC and record-keeping. In lending, we might see a consortium of banks maintaining a shared KYC or credit ledger on blockchain in the coming years. This would make the verification APIs even more powerful – queries would yield trustworthy results in seconds, with no single point of failure or risk of data tampering. As Perfios noted, the integration of blockchain will ensure tamper-proof records and elevate security in verification.

Unified Lending Interfaces & Open Banking Expansion: We’re also witnessing the rise of unified platforms (sometimes regulator-led) that bring multiple verifications under one roof. The RBI’s Unified Lending Interface (ULI), just launched in 2024, is an open platform that connects lenders to various databases through open APIs – Aadhaar e-KYC, PAN, land records, account aggregators, etc., all in one system. This kind of orchestration can massively streamline verifications. ULI essentially provides a plug-and-play API hub for all the key checks needed for credit underwriting, accessible to banks and NBFCs. It’s being likened to how UPI created a unified payments ecosystem. As Governor Shaktikanta Das said, “just like UPI transformed payments, ULI will play a similar role in transforming lending in India” (India’s central bank launches lending platform connected to Aadhaar KYC | Biometric Update). In the future, we can expect ULI to mature and possibly incorporate even more data sources (maybe GST, vehicle registrations, court records for legal case checks, etc.). This means a bank integrating with ULI might get one-stop access to all verification needs – greatly simplifying implementation. It’s an example of the innovation in digital public infrastructure that India is spearheading, and it will push the envelope on how efficiently lending can be done.

Central Bank Digital Currency (CBDC) Integration: With the advent of the Digital Rupee (India’s CBDC) pilot, new lending models might emerge where loans could be disbursed and repaid in digital currency. Verification APIs will adapt to this by linking with CBDC systems. For instance, if a borrower holds a CBDC wallet, an API might allow a lender (with permission) to verify the identity linked to that wallet (since wallets will be KYCed) and even view wallet transaction history (which could serve as another source of repayment capacity information). Additionally, smart contract-based loans could become possible: a loan agreement in code that automatically pulls verification info and executes disbursement/repayment conditions. In such cases, verification APIs would feed the smart contract with off-chain data (via oracles) – e.g., confirming that collateral is registered or income remains above a threshold, triggering certain clauses. While these are nascent ideas, APIs will be the connectors between traditional banking systems and new digital currency platforms. They will ensure that even as money itself becomes software, the necessary checks and balances (KYC, creditworthiness, etc.) keep pace in real-time. CBDCs could also facilitate more inclusive lending (microloans via mobile, etc.), and APIs will be there to instantly verify borrower identity for even a ₹500 loan initiated in a digital rupee app.

New Data Sources and Alternative Credit Models: Looking forward, lenders will continue to seek alternative data to underwrite loans for those with no formal credit history. Verification APIs might expand to include things like telecom data (to verify phone bill payment behavior), utility payment records, educational records (to verify credentials for student loans), and even social media or e-commerce data (with all due privacy considerations). TartanHQ is already providing APIs for some of these – for example, an API that can verify someone’s employment by their work email domain. As financial services blur into tech, the definition of what needs to be verified will broaden, and APIs will be at the heart of exchanging this information quickly. In the future, even peer-to-peer lending and BNPL (Buy Now Pay Later) ecosystems could use shared verification APIs. Imagine a P2P lending platform where, with the borrower’s consent, the platform’s API verifies the person’s identity and salary with a bank and shares that verification with individual lenders as a token of trust. Essentially, every participant in the credit value chain might tap into verification APIs to make real-time, informed decisions.

In summary, the next wave of innovation will make verification more intelligent, more decentralized, and more ubiquitous. AI will add brains to the operation, blockchain will add security and shared trust, and broader API platforms will make access universal. The outcome could be truly real-time lending decisions – loans approved as fast as a UPI payment, with a high degree of confidence in the borrower’s identity and intent to repay. Banks that stay ahead of these trends (perhaps by working with fintech partners on pilots in AI/ML underwriting or joining industry blockchain KYC consortia) will be well-positioned. The common theme is that APIs are the future-proof way to plug into new technologies. They allow banks to embrace innovation at a pace that suits them, by modularly adding capabilities. So as the landscape evolves – from classical databases to AI models and distributed ledgers – banks that have built an API-first architecture can readily integrate these future tools and continue delivering quick, secure loans to customers in the digital age.

Conclusion

Verification APIs have undeniably become the linchpin of modern lending operations in India. They enable banks and fintech lenders to make credit decisions with greater speed, accuracy, and confidence than ever before. By automating identity checks, income and asset verification, and compliance workflows, APIs allow loan processing that once took weeks of back-and-forth to be completed in a matter of minutes or hours. This not only delights customers (who get faster approvals and disbursements) but also strengthens the lender’s portfolio by reducing fraud and human error. We’ve seen how Indian banks are leveraging everything from Aadhaar and PAN verification to account aggregator data and credit score APIs to paint a full picture of the borrower instantly, adhering to all regulatory requirements in the process. The business case is clear – faster onboarding, lower operational costs per loan, and improved risk management. No wonder even traditional banks have begun partnering with API providers like TartanHQ to modernize their systems and stay competitive in the fintech era.

In essence, verification APIs are transforming lending decisions from a manual art into a digital science. They encapsulate the best of digital transformation – speed, scalability, and data-driven precision – while keeping the process secure and compliant. As we move forward, these APIs will only grow more powerful with AI and broader integrations, heralding innovations like predictive credit analytics and blockchain-based trust networks. Banks that embrace this API revolution will be able to respond to customer needs in real-time, launch new products faster, and extend credit to previously underserved segments safely. It’s an exciting time where technology and finance converge to make lending more inclusive and efficient.

Pramey Jain

CEO & Founder